Press Release Archive

2024

Venbrook's Student Insurance Names Jessica MacDonald Vice President SalesVenbrook Wholesaler, Brooks Insurance, Strikes Alliance with CoverForce for On-Demand Quote & Bind API Platform

Venbrook Deepens the Bench with Christopher Harney to Grow Real Estate and Healthcare Divisions

Venbrook Group Recognized With 2023 Cigna Healthy Workforce Designation

Venbrook's Carl Warren & Company Celebrates 50 Years as a Third Party Administrator

Venbrook's Student Insurance Expands Exclusive Partnership with Anthem Blue Cross to Bring Accident Insurance to Universities Across California

Venbrook Adds to Senior Leadership Roster, Appoints Brooke Lais as Chief Marketing Officer

2023

Venbrook Launches National Higher Ed Division To Deliver Complete Risk Management Solutions for Schools, Students, And Staff; Alison Myers At The HelmVENBROOK, A 13+ YEAR TMPAA MEMBER, PROVIDES A STRONG PRESENCE AT MEMBER-EXCLUSIVE TARGET MARKETS’ 23RD ANNUAL SUMMIT

Venbrook and InterContinental Insurance Brokers Announces Promotions and Expansion of Private Client Services Division

Venbrook Insurance Services Strengthens Commercial Retail Services Segment Nationally With Two New Vice Presidents

Venbrook Bolsters Services Division With Two New Verticals, Names Thomas E. Sleeper Practice Leader To Meet Rising Demand Across U.S.

Brooks Insurance Agency, 15+ Year Exhibitor, Sponsor, And 20+ Year PIA Member, At Premier Industry Leading Insurance Event, Professional Insurance Agents 2023 Annual Conference

Student Insurance Attends 2023 Association Of Chief Business Officials Spring Conference, Celebrates 20th Year As A Gold Sponsor Of Annual Event

Venbrook Names Juan Aguilar New Chief Financial Officer

Student Insurance Unveils New Brand Identity And Website To Celebrate 70 Year History Of Offering Student And Academic Healthcare Plans

Carl Warren & Company Attends RIMS RISKWORLD 2023 Alongside The Best Providers In Risk Management

Venbrook Strengthens Management Team, Promotes Brenda Sherman To Executive Vice President Of Business Development And Strategic Alliances

Venbrook Appoints Bryan Meyer Executive Vice President And Head of U.S. Programs Division

2022

Suzie Spencer Promoted to Vice President of Business DevelopmentVenbrook Names Louis Pippin Chief Claims Officer To Expand Third Party Administration Capabilities Across The Country And Internationally

Venbrook Names Jeff Lang Executive Vice President, Retail Services Practice Leader

Venbrook Names Jack Reddy Chief Human Resources Officer

Louis Pippin, Chief Claims Officer, featured in a The Defense Never Rests podcast interview with Morgan & Akins, PLLC

2021

Venbrook Bolsters East Coast Presence with Acquisition of InterContinental Insurance BrokersVenbrook Group Acquires Alpharetta Underwriters

Venbrook Partners with Jason Allen of Worldwide Risk Management to Grow U.S. Government Contractor Insurance Practice

Venbrook Acquires RD Parisi and David Morse and Associates to Bolster Employee Benefits and Claims Services

CONSTRUCTION COSTS AND INSURABLE VALUES: ENSURING COVERAGE ADEQUACY WHILE CONTROLLING PREMIUM COST IMPACT

Venbrook Partners with Everspan on a Non-Emergency Medical Transportation Program

2020

2019

East Coast Meets West Coast as Brooks Insurance Agency Announces Expansion2018

Venbrook Insurance Services Announces Promotion of Tim Johnston to Managing Director of Construction Division2017

Brooks Insurance Agency Partners with The Hartford on Third-Party Logistics Warehouse PracticeWestlake Risk & Insurance Services Partners with Benefits America

2016

Venbrook Group, LLC Secures $42M from Madison Capital FundingClean Cash Flow™: How you can take advantage of financial and tax incentives to generate new revenue from your commercial real estate.

Venbrook targets wholesale expansion after fundraise.

CONSTRUCTION COSTS AND INSURABLE VALUES: ENSURING COVERAGE ADEQUACY WHILE CONTROLLING PREMIUM COST IMPACT

CONSTRUCTION COSTS AND INSURABLE VALUES: ENSURING COVERAGE ADEQUACY WHILE CONTROLLING PREMIUM COST IMPACT

Over the last few years, property insurance carriers and lenders have asked many insureds to raise the building values of select assets. Without question this has immediate and direct ramifications for these buildings’ insurance costs (premium = rate * value), which can both be frustrating and seemingly arbitrary. Here’s some background on why this is happening and what you can do about it.

UNDERSTANDING THE TERMS “AGREED VALUE” AND “REPLACEMENT COST”

Under a property policy, the two terms “agreed value” and “replacement cost” are critical and likely familiar to those who routinely review loan covenants. Agreed value simply states that the insurance carrier consents to underwrite the property value that the insured has provided, without any applicable coinsurance provisions. Briefly, coinsurance essentially creates a coverage penalty if the carrier determines that the declared value is insufficient at the time of loss. This doesn’t apply under an agreed value structure.

The heart of the matter here is replacement cost, because it defines both the insured’s and the insurer’s responsibilities. A replacement-cost policy reimburses “the cost to rebuild or replace on the same site with new materials of like size, kind and quality.” This AFM policy definition is fairly standard across ISO and other carrier forms, and the emphasis is ours. Critically, this does not deduct any depreciation as an actual cash-value provision would. As a condition of coverage, prior to the policy term, the insured is responsible for providing a good faith estimate of the likely replacement cost for each building insured.

CONSTRUCTION COSTS HAVE SKYROCKETED

If constructing or renovating a building today at any scale, costs have skyrocketed in recent months. At last look, lumber was up roughly 200 percent year over year. Steel prices and labor costs are higher too, and this all has a direct impact on the actual cost to rebuild an existing building using new materials. If the building suffered a loss today, carriers would be on the hook for those escalated costs and, as such, now are looking for insureds to increase reported values so carriers can charge appropriate premiums. In many instances, even recent improvements may be revalued though they were built only within the last year or two, which shows how quickly the market has escalated. It’s simply more expensive to build today than even just a few months ago. This drives the carriers’ positions, unfortunately, as they tend to see their own claim/reconstruction costs increasing on a per-square-foot basis.

Many lenders also pay close attention to their collateral property valuations. A limit that may have been sufficient in the past now in fact may be underinsuring the same property given escalating costs. Similarly, many insureds have a fiduciary duty to third-party investors or even extended family members to maintain adequate insurance on portfolio properties. This also requires taking a closer look at how the property is valued.

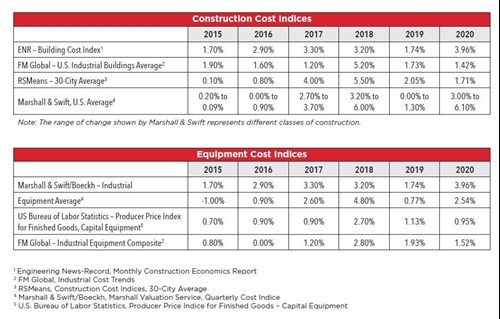

In practice, carriers are paying more attention to this than in years past but, typically, they leave room for negotiation. Ultimately, a replacement cost is subjective to at least some degree, and stakeholders must understand the acceptable range. Most carriers use Marshall & Swift to run a benchmark report for the property, which, again, models based on today’s construction costs. They require all insureds to come within a fixed percentage of the benchmark – typically 20 to 30 percent.

We also run these reports on our clients behalf and typically use them to benchmark portfolio values. Carriers will consider a detailed counterpoint as well. It could take the form of a building replacement-cost appraisal or engaging with a third-party service such as Duff & Phelps, a valuation-service provider that most carriers accept and who provided the benchmark data below (Cost Trend Update Bulletin - March 2021). Of course, commissioning a study like this also risks producing a higher value than the one the carrier offers.

ALLOCATIONS: SPREADING THE IMPACT ACROSS A PORTFOLIO

Venbrook works with carriers to mitigate the cost impact to clients. Typically we’re successful in limiting the revaluation to small portions of a portfolio at a time, or applying nominal, “inflationary” adjustments to portfolios rather than wholesale increases in lockstep with construction-cost benchmarks. This still may cause a shock, however, when even one to three buildings see substantial increases in value, year over year, and owners pass this cost through to property-level accounting. This often leads to tenant calls questioning the swings in passed-through amounts. As always, allocations are more art than science and sometimes the impact can be spread across a portfolio.

A true blanket loss limit, without margin or so-called “statement-of-values” clauses, can be an effective tool to mitigate the risk of underreported values so long as a carrier agrees to the declared values. Most at risk in this inflationary environment are those with policy language directly limiting available policy limits to some function of declared values. With construction costs escalating at this pace, values declared at the start of a policy term may no longer be sufficient in practice.

How this affects you depends on carrier, portfolio, and the buildings themselves. We’re always available to discuss further and provide additional detail.

About Venbrook®

Venbrook Group, LLC is a holding company with subsidiaries engaged in retail broking, wholesale broking, programs, and claims services. Venbrook caters to a national client base across myriad industries with divergent needs. Venbrook's team of experts and industry specialists partner with their clients to manage their risks, create security, promote growth, and add value by delivering best-in-class insurance products and programs. Venbrook is headquartered in Los Angeles, with various locations across the country.

For more information, please visit www.venbrook.com

Media and Press Release Inquiries:

Rhonda Turner

Tel: 408-316-9077 | rturner@venbrook.com

Follow our community:

LinkedIn – www.linkedin.com/company/venbrook

Facebook – www.facebook.com/venbrook

Twitter – www.twitter.com/venbrook